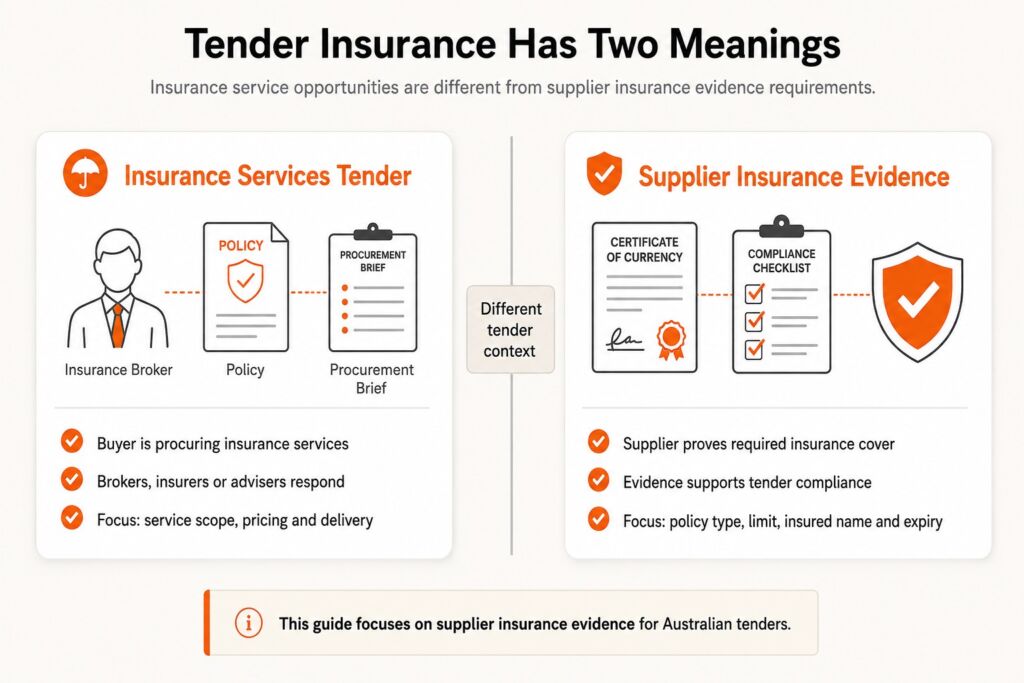

Tender insurance in Australia has two practical meanings: insurance tenders where buyers procure insurance services and insurance requirements that suppliers prove when bidding for other work. This guide focuses on supplier insurance evidence for Australian tenders while separating that topic from financial and insurance services opportunities. It explains policy types, timing, certificates of currency, coverage limits, tender-response mapping, capability statement support, common non-compliance risks and pre-submission insurance checks.

What Does Tender Insurance Mean in Australia?

Tender insurance in Australia means either a tender to supply insurance services or the insurance evidence a supplier provides in a tender response. The second meaning is the main compliance issue for contractors, consultants, service providers and product suppliers bidding for government or private work.

- Insurance tender opportunities are RFT, RFQ, EOI or RFP documents where a buyer procures insurance broking, risk advisory or financial services.

- Tender insurance requirements are policy conditions, certificate requests and coverage evidence that a supplier provides for another contract.

- Supplier compliance evidence usually includes certificate of currency details, policy type, insured entity, limit of cover and expiry date.

- Procurement risk controls use insurance to address liability, injury, advice risk, property damage and contract-performance exposure.

The tender documents decide which meaning applies to the live opportunity.

Is Tender Insurance About Insurance Tenders or Insurance Requirements?

Tender insurance is about both insurance tenders and insurance requirements, but this page focuses on supplier insurance requirements. Insurance-tender opportunity pages help insurers, brokers and financial services firms find contracts. Supplier insurance requirement pages help businesses prove current cover for a construction, consulting, supply or services tender.

The distinction matters because an insurance provider selling cover answers a different tender from a contractor proving cover.

Why Do Tenders Ask for Insurance?

Tenders ask for insurance because buyers use policy evidence to manage legal liability, workplace injury, professional advice, property damage, construction risk and contract-performance exposure. Insurance does not prove capability by itself, but it reduces the buyer’s uninsured loss risk.

- Public liability manages third-party injury and property damage risk created by site work, services or public-facing activity.

- Professional indemnity manages financial loss from professional advice, design, consulting, broking or specialist services.

- Workers compensation manages workplace injury obligations where employees perform contract work.

- Contract works insurance manages damage to works, materials and site assets during construction or infrastructure delivery.

- Product liability manages injury or damage caused by supplied products, equipment or materials.

- Plant or equipment insurance manages damage, theft or operational risk linked to nominated project assets.

The tender response needs to show the policy type that matches the contract risk. Irrelevant policy evidence rarely satisfies a mandatory insurance schedule.

When Does a Supplier Need Insurance for a Tender?

A supplier needs insurance for a tender when the tender conditions, evaluation process, contract award or contract commencement requirements ask for current policy evidence. Some Australian government guidance indicates insurance is often not required until award, but the tender document controls the live requirement.

- Tender lodgement: the buyer requests certificates, declarations or policy details with the submission.

- Evaluation: the buyer checks whether the supplier has appropriate cover before shortlisting or negotiation.

- Preferred-supplier stage: the buyer asks for current certificates before award.

- Contract award: the supplier provides required policies as an award condition.

- Contract commencement: the supplier confirms cover before site access, service delivery or project mobilisation.

The safest response method is to identify each insurance reference in the RFT, contract conditions, schedules and addenda before pricing or final lodgement.

What Types of Insurance Are Commonly Requested in Tenders?

Tender insurance requirements commonly include public liability, professional indemnity, workers compensation, contract works, product liability and project-specific cover. The required policy set depends on the work scope, buyer policy, contract wording and risk level.

| Insurance type | Risk covered | Common tender trigger |

| Public liability | Third-party injury and property damage | Site visits, works, services, events, public interaction or property access |

| Professional indemnity | Advice, design, consulting or professional-service errors | Consulting, engineering, design, broking, financial or advisory services |

| Workers compensation | Employee workplace injury | Employees performing work under the contract |

| Contract works | Damage to construction works and materials | Building, infrastructure, civil works or construction projects |

| Product liability | Injury or damage caused by supplied products | Goods supply, equipment, materials or manufactured items |

| Plant and equipment | Damage, theft or loss involving nominated assets | Plant-heavy works, hired equipment or project-specific machinery |

The tender schedule usually names the required class of insurance and minimum evidence standard.

What Public Liability Insurance Is Needed for Tenders?

Public liability insurance for tenders covers third-party injury and property damage linked to the supplier’s business activities under the contract. The tender conditions specify the required coverage limit, insured entity, certificate evidence and any contract-specific wording.

A supplier avoids assuming one standard amount. Public liability limits change by contract value, site exposure, public interaction, buyer policy and risk category. The current certificate of currency shows the insured entity, policy period, insurer and limit requested by the buyer.

When Is Professional Indemnity Required in a Tender?

Professional indemnity is required in a tender when the supplier provides advice, design, consulting, broking, engineering, financial or professional services that create advice-related loss risk. The policy responds to professional error, omission or breach connected to specialist work.

Relevant examples include design consultants, engineers, architects, insurance brokers, financial advisers, project managers and technical consultants. A tender that only involves physical supply or basic labour often excludes professional indemnity unless the contract documents request it.

Do Tenders Require Workers Compensation Insurance?

YES, tenders commonly require workers compensation insurance when the supplier employs workers or the tender conditions request evidence of statutory workplace insurance. Requirements vary by state, business structure, work type and contract conditions.

Workers compensation evidence usually matters when staff perform contract work, enter buyer sites or deliver services under the supplier’s employment structure.

What Insurance Is Needed for Construction Tenders?

Construction tenders need insurance that matches site risk, works damage, worker safety, third-party liability, product risk and professional design exposure. The buyer, contract form and project risk profile set the final policy list.

- Contract works insurance for damage to works, materials and temporary structures.

- Public liability insurance for third-party injury or property damage.

- Product liability insurance for supplied materials, fixtures or equipment.

- Workers compensation insurance for employees performing project work.

- Professional indemnity insurance where design, advice, engineering or certification services are included.

- Plant and equipment insurance where nominated machinery, vehicles or hired equipment create project exposure.

Construction insurance evidence needs checking against the contract conditions before the supplier confirms compliance.

What Insurance Documents Are Needed for a Tender?

Tender insurance documents usually include current certificates of currency, policy schedules, endorsements, declarations and insurer details that prove the required cover exists. Buyers check the evidence against the tendering entity, policy class and contract conditions.

- Certificate of currency: confirms policy class, insured party, insurer, period of cover and coverage limit.

- Policy schedule: shows policy structure, named insured parties, extensions, exclusions and applicable limits.

- Endorsements: prove special contract wording, principal noting or project-specific terms where required.

- Insurer details: identify the underwriting insurer or broker contact requested by the buyer.

- Policy number: connects the certificate to a live insurance contract.

- Insured entity: confirms the legal entity submitting the tender is covered.

- Expiry date: proves the policy remains current through evaluation, award or commencement.

- Coverage limit: confirms the policy meets the minimum value in the tender documents.

- Insurance declarations: confirm that the supplier holds required cover or plans to obtain it at the required stage.

Each file is named clearly and mapped to the relevant tender schedule or compliance criterion.

How Much Insurance Cover Is Needed for a Tender?

The insurance cover needed for a tender is the amount stated in the tender documents, buyer policy, contract conditions or risk assessment for the work type. No single coverage amount applies to every Australian tender.

Use this method to check coverage limits:

- Read the insurance clause in the RFT, draft contract and response schedules.

- Record each policy type and minimum coverage amount in the compliance matrix.

- Compare the required limit against the certificate of currency and policy schedule.

- Check whether the limit applies per claim, in aggregate or for a project period.

- Confirm any contract-specific endorsements, principal noting or additional insured wording.

- Ask an insurance broker to review unusual limits, exclusions or construction clauses.

How Is Insurance Shown in a Tender Response?

Insurance is shown in a tender response through a mapped evidence trail that links each required policy to the schedule, compliance matrix, certificate and contract condition. The evaluator needs to find the required proof without interpreting scattered attachments.

- Add every insurance requirement to the compliance matrix.

- Complete the insurance schedule with policy type, insurer, policy number, limit and expiry date.

- Attach current certificates of currency in the requested file format.

- Add policy schedules or endorsements where the buyer requests more than a certificate.

- Identify any coverage gaps as a contract departure or award condition only where the tender permits that approach.

- Name attachments using the tenderer’s legal entity, policy type and expiry date.

- Check that insurance evidence matches the entity named in pricing, declarations and contract schedules.

How Does a Capability Statement Support Tender Insurance Evidence?

A capability statement supports tender insurance evidence by summarising current policy types, coverage status, insurer details and certificate availability in one supplier profile. It helps the evaluator see insurance readiness before reviewing attachments.

- Public liability status and coverage limit

- Professional indemnity status where relevant

- Workers compensation status for employees

- Contract works or product liability status where relevant

- Certificate availability and policy expiry dates

- Legal entity, ABN and contact details

The capability statement supports the tender response, but it does not replace certificates of currency or required schedules.

How Are Insurance Tenders Different From Tender Insurance Requirements?

Insurance tenders differ from tender insurance requirements because one involves selling insurance services to a buyer and the other involves proving insurance compliance as a supplier. The exact keyword SERP contains both meanings.

| Topic | Insurance tenders | Tender insurance requirements |

| Searcher goal | Find or respond to contracts for insurance, broking or financial services | Understand what cover a supplier needs for a tender |

| Buyer role | Procures insurance services or risk advisory support | Checks supplier risk, liability and contract compliance |

| Supplier role | Insurance broker, insurer, claims adviser or financial services provider | Contractor, consultant, product supplier or service provider |

| Documents | Service proposal, pricing, claims model, broking methodology and industry credentials | Certificates of currency, schedules, endorsements, declarations and compliance matrix |

| Content focus | Winning insurance-sector work | Meeting insurance evidence requirements in a tender response |

This article stays focused on supplier compliance while acknowledging that opportunity portals also rank for the keyword.

What Insurance Mistakes Cause Tender Non-Compliance?

Insurance mistakes cause tender non-compliance when they create invalid evidence, wrong policy matching, entity mismatch, insufficient cover or missing mandatory documents. Each mistake needs a direct prevention step before lodgement.

- Expired certificate: replace certificates before submission and check expiry against the required evaluation or award date.

- Wrong legal entity: confirm the insured party matches the tendering entity, ABN and declarations.

- Insufficient cover: compare policy limits against the exact amounts stated in the tender documents.

- Missing workers compensation: provide statutory workplace insurance evidence where employees perform contract work.

- Wrong policy type: avoid using public liability to answer professional indemnity, contract works or workers compensation requirements.

- Missing endorsement: attach principal noting, additional insured wording or project-specific endorsement where requested.

- Ignored contract wording: check whether the draft contract requires cover beyond the response schedule.

- Unclear file naming: label certificates by legal entity, policy type and expiry date.

- Unsupported declaration: avoid declaring future insurance cover unless the tender allows award-stage evidence.

- No broker review: get policy wording checked when the contract contains unusual exclusions, high limits or construction risk.

How Do Suppliers Check Insurance Before Submitting a Tender?

Suppliers check insurance before submitting a tender by matching every policy requirement to the tender schedule, insured entity, coverage limit, expiry date, certificate and contract wording. This is the final insurance evidence check before lodgement.

- Policy type: confirm each required class, such as public liability, professional indemnity, workers compensation or contract works.

- Insured entity: match the certificate to the legal entity submitting the tender.

- Coverage limit: compare every required amount with the certificate and policy schedule.

- Expiry date: confirm policy currency through the relevant tender, award or commencement stage.

- Tender schedule: complete each insurance field with consistent insurer, policy number and limit details.

- Contract wording: check principal noting, additional insured wording, exclusions and endorsements.

- Broker advice: obtain review for high limits, construction risks, professional indemnity concerns or unusual contract clauses.

- Attachment upload: name each file clearly and confirm the portal upload includes all certificates.

- Award timing: note any cover to be obtained before contract award or commencement where the tender permits it.

The closing check loops back to the opening issue: tender insurance evidence proves procurement risk control through current policies, certificates of currency and clear compliance mapping.

When Does a Supplier Get Insurance Advice Before Tendering?

A supplier gets insurance advice before tendering when the contract wording, required limit, policy exclusion, professional indemnity exposure or construction risk is unclear. Broker or legal review is useful before the supplier declares compliance.

- High coverage limits or unusual deductibles

- Construction, plant, site or contract works exposure

- Professional indemnity conditions for advice, design or certification

- Principal noting, additional insured or waiver requirements

- Policy exclusions that conflict with tender conditions

- Award-stage insurance that affects price or risk allocation

Advice occurs before final pricing and before insurance declarations are signed.

Is a Supplier Able to Submit a Tender Before Buying the Required Insurance?

YES, in many cases a supplier is able to submit before buying the required insurance, but the tender often requires evidence during evaluation, at preferred-supplier stage, before award or before contract commencement. The tender conditions decide the timing.

The response states current cover, planned cover or award-stage evidence only where the tender documents allow that approach.

Does a Certificate of Currency Match the Tendering Entity?

YES, the certificate of currency matches the tendering legal entity or clearly shows that the tendering entity is covered by the policy structure. Entity mismatch creates a compliance risk when the buyer compares certificates with the ABN, declarations and contract schedules.

Trading names, group policies and subcontracting structures require careful evidence review.

Does Public Liability Insurance Replace Professional Indemnity Insurance?

NO, public liability insurance does not replace professional indemnity insurance because the policies cover different risks. Public liability deals with third-party injury or property damage. Professional indemnity deals with advice, design, consulting or professional-service errors.

A tender that requests both policy types needs separate evidence unless the buyer permits a different arrangement in writing.

Is Workers Compensation Required for Sole Traders With No Employees?

NO, workers compensation is usually not required for a sole trader with no employees, but the answer depends on state rules, subcontractor status, engagement model and tender conditions. This section is not legal advice.

The supplier checks the relevant state requirements and the tender schedule before declaring that workers compensation is not applicable.

Is a Tender Rejected for Expired Insurance Evidence?

YES, a buyer rejects or delays a tender when current insurance evidence is mandatory and the supplier submits an expired certificate of currency. The risk is highest when insurance evidence is a mandatory schedule, award condition or contract commencement requirement.

Current certificates, correct insured entity details, coverage limits and policy expiry dates form the minimum evidence trail for tender insurance compliance.